Life insurance confuses most people. Too many options. Complicated terms. Sales agents are pushing different plans.

Two common ones are term plans and endowment plans. They sound similar but work completely differently.

Understanding Endowment Plan

An endowment plan is insurance plus savings mixed together. You get life cover, and you also build money over time.

Pay premiums for 15 or 20 years. If you die during this time, your family gets the sum assured. If you survive, you get all that money back with bonuses added. This is the endowment plan in a nutshell.

What makes endowment plans different:

- Life protection and savings in one package

- Get money back even if nothing bad happens

- Premiums are much higher than pure insurance

- Maturity benefits after the policy period ends

- Bonuses get added yearly

Think of it as forced savings with insurance attached. The insurance company invests your premium. Gives you returns later.

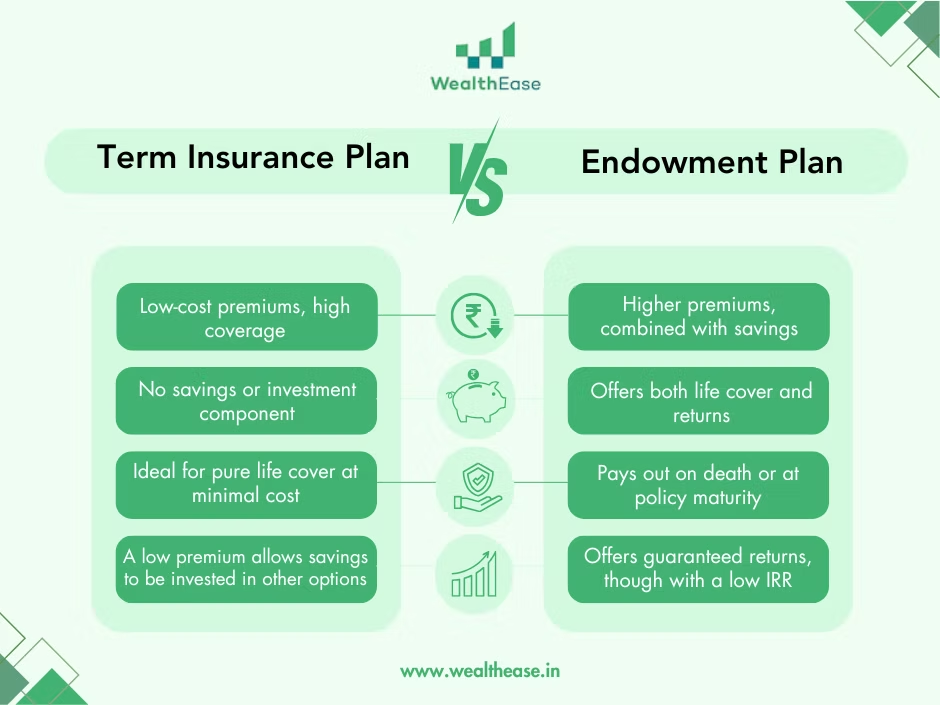

What Are Term Plans?

Term plans are pure life insurance. Nothing else. No savings. No maturity benefits. Just protection.

You pay premiums. If you die during the policy term, your family gets the money. If you survive, you get nothing back. Zero.

Sounds harsh, but there’s a reason people love term plans. They’re incredibly cheap. Same coverage costs way less.

The Term Plan Premium Calculator Tool

A term plan premium calculator helps you figure out costs before buying. Simple online tool. Enter some details. Get instant premium quotes.

What you typically enter:

- Your age and gender

- How much coverage you need

- Policy duration you want

- Smoking habits

- Any existing health issues

Within seconds, you see what you’ll pay monthly or yearly. Compare different coverage amounts easily.

Super helpful for planning your budget. No surprises later.

Why Endowment Plan Meaning Matters Here

Here’s where people mess up. They use a term plan premium calculator, expecting endowment plan features. Doesn’t work that way.

The confusion happens because:

- Both offer life coverage

- Both need regular premium payments

- Both protect your family

- Names sound insurance-related

- Agents sometimes mix them up intentionally

But the premium calculator shows term plan costs only. Those numbers don’t apply to endowment plans at all.

The Huge Price Difference

This is critical. Endowment plans cost 6 to 10 times more than term plans for the same coverage.

Let’s use real numbers. Say you’re 30 years old. You want 50 lakh coverage for 30 years.

A term plan might cost you 8,000 yearly. An endowment plan for the same coverage? Around 60,000 yearly. Massive gap.

Why? Because endowment plans are doing two jobs. Insurance plus investment. Term plans do not provide insurance.

When the Calculator Misleads You

People check the term plan premium calculator. See affordable numbers. Get excited. Then visit an agent.

The agent pushes an endowment plan instead. Shows you’ll get money back. Sounds great. You agree.

Later, you realise the premiums are crazy high. Too late. You’re locked in.

This happens because:

- The calculator showed term plan rates

- You didn’t understand endowment plan meaning clearly

- Agent focused on returns, not costs

- You assumed all insurance costs the same

- The maturity benefit sounded attractive

Understanding both helps you compare properly. Apples to apples.

What Each Plan Actually Does

Term plans give you:

- Maximum coverage for minimum cost

- Pure risk protection

- Flexibility to invest savings elsewhere

- Simple, straightforward structure

- Easy to understand

Endowment plans give you:

- Guaranteed maturity benefits

- Forced savings discipline

- Lower coverage for higher premiums

- Mixed insurance and investment

- Complicated bonus structures

Neither is bad. They serve different purposes. But knowing the difference prevents expensive mistakes.

Making Smart Decisions

Use the term plan premium calculator for what it’s made for. Checking term plan costs. Not estimating endowment premiums.

If you want endowment plan quotes, ask specifically for those. The calculator won’t help there.

Before deciding anything:

- Understand your actual insurance needs

- Calculate how much coverage your family needs

- Check what you can afford monthly

- Compare both plan types properly

- Don’t mix up features and costs

Most financial experts suggest buying term plans for insurance. Invest the premium difference separately. Usually works out better.

Common Mistakes People Make

Buying an endowment plan,s thinking they’re getting term plan prices. The shock comes at payment time.

Not using calculators at all. Just trusting agent quotes. Always verify independently.

Focusing only on returns from endowment plans. Ignoring that insurance coverage is actually low for the premium paid.

Assuming expensive means better. Higher premiums don’t automatically mean better protection.

Getting term insurance and then stopping because they didn’t get money back. That’s not how term plans work.

The Right Way to Use Calculators

Start with clear goals. How much coverage does your family need if something happens to you?

Factor in debts, daily expenses, children’s education, everything. Be realistic.

Then use a term plan premium calculator to see costs. Try different coverage amounts. Different policy lengths.

Compare multiple options. See what fits your budget while giving adequate protection.

If you want savings too, calculate separately. Don’t bundle everything into one endowment plan without understanding costs.

Real World Example

Rajesh is 35. Has two kids. Needs 1 crore coverage. Uses a term plan premium calculator. Sees he’ll pay around 15,000 yearly.

Perfect. He can afford that. Then his agent shows an endowment plan. Same 1 crore coverage. But wait.

Premium is 1.2 lakh yearly. Eight times more. Rajesh can’t afford it. So the agent reduces coverage to 20 lakhs to fit his budget.

Now Rajesh has way less protection. His family is at risk. All because he didn’t understand the endowment plan before using the calculator.

Bottom Line

The term plan premium calculator is a fantastic tool if you know what you’re calculating.

Understanding the endowment plan’s meaning prevents confusion and helps you compare correctly. Stops you from making costly mistakes.

Use calculators. Ask questions. Read policy documents. Don’t rush decisions involving lakhs of rupees. Your family’s protection is serious business.